The Thrift Savings Plan offers Federal Employees and Uniformed Services personnel the same types of tax benefits and savings as most private-sector 401(k)s.

Every pay-period, the agency you work for deposits 1% of your basic pay into your TSP. Then, you have the option of making additional contributions; your agency will match up to 5% of your contributions, making this an ideal plan for saving for retirement.

The TSP isn’t a pension plan (like FERS), it’s a savings plan that is meant to offset the very basic things that FERS will not cover.

Saving well in your TSP account, with the government providing up to a 5% contribution, means that you will have money that you can roll out of the TSP to sustain your lifestyle needs and wants in retirement. If at all possible, we recommend choosing to contribute 5% to your TSP, as this will guarantee an automatic 100% rate of return while you are a full-time Employee. The 2025 contribution limit is $23,500; additionally, employees aged 50 or older can fund make-up contributions up to $7,500.

Remember, this is not a pension fund, it’s an annuity/investment that you can move from its government-controlled TSP plan into a plan that provides you a combination of growth, security, and if you want – the option of having an assured life-time monthly income.

- Your TSP savings are yours to control, without penalty after the age of 59.5 or one-month following severance (allowing your final TSP deposit to clear).

- How it works – when you make a no-penalty/no-tax rollover of your TSP (group-controlled 401K) into a self-directed IRA, you immediately have greater control not only over your investments, but also over your withdrawals during retirement. You worked hard for your savings – now let your money work for you.

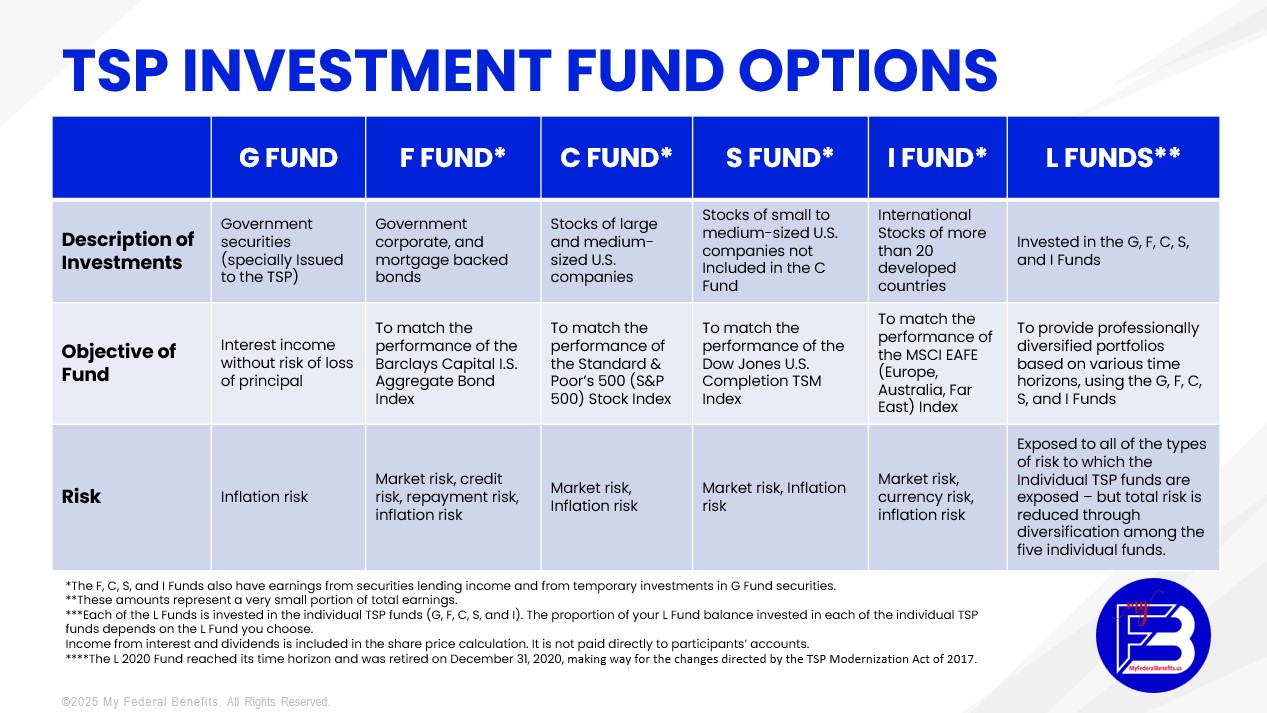

When you set up your TSP account, you’ll have three investment options:

- Individual TSP Funds. There are five: the G, F, C, S, and I Funds that include everything from U.S. Treasury securities to stocks and bonds.

- Lifecycle Funds. There are 11 L-Funds: each includes a mix of the five individual TSP funds. You can choose to invest your entire portfolio in a single L Fund.

- Mutual Funds. Provided that you meet certain eligibility-requirements and pay the necessary fees, you can choose to place your TSP savings in a mutual funds.

When you get ready to withdraw your money from the TSP, you’ll be taxed based on the type of contributions you made and how you withdraw your savings.

If you have a Traditional TSP, your “non-qualified” contributions were made pre-tax, so withdrawals are fully taxable under your Federal Income Tax, and possibly when you pay your state taxes; this includes a 20% mandatory Federal Tax withholding unless your funds are rolled into another self-directed IRA. Additional penalties exist for withdrawing funds before age 59.5 (or age 50 for Federal Employees covered by special provision). Federal Experts can provide you with a complimentary Benefits Analysis so you can see where your money is, where you want it to be, while choosing how you want to secure your future and keep your tax impact as low as possible.

If you have some of your TSP savings in a Roth TSP, because contributions were made after-tax (and thus are considered “qualified”), and you’ve had your account for at least 5-years and are at least 59.5-years old, you’ll be able to withdraw your money 100% tax-free.

By age 73, there are required withdrawals (Required Minimum Distributions/RMDs – per the SECURE 2.0 Act). The Required Minimum Distribution (RMD) includes a calculation, but roughly requires a withdrawal of 4.5% annually.

- RMDs apply to tax-advantaged retirement accounts: TSP, Federal Employee’s Annuity, Traditional IRAs including SEP IRAs & SIMPLE IRAs, 401(k) Plans including traditional 401(k)s & solo 401(k)s, 403(b) Plans, 457(b) Government Plans, Inherited IRAs, both Traditional & Roth and Inherited Employer-Sponsored Retirement Plans.